FINANCIAL ACCOUNTING TOPIC 8 REVENUE AND EXPENSE RECOGNITION REFERENCE

BRIEF GUIDE TO THE FINANCIAL MANAGEMENT COMPETENCIES NEEDEDCOURSE TITLE BUS030150FINANCIAL ACCOUNTING BRIEF DESCRIPTION

FORMA PARA AYUDA FINANCIAL EL WOMEN’S WILDERNESS INSTITUTE

Public non Financial Corporations Community Service

(6030154) 5 N240(E)(M31)H NATIONAL CERTIFICATE COMPUTERISED FINANCIAL SYSTEMS N4

0 REGISTRATION OF LORDS’ FINANCIAL AND OTHER INTERESTS

Concept 8

FINANCIAL ACCOUNTING

Topic 8: Revenue and Expense Recognition

Reference: Kimmel, Paul. D., Weygandt, Jerry. J. & Kieso, Donald. E. (2006). Financial Accounting: Tools for Business Decision Making (4th ed.). Hoboken, NJ: John Wiley & Sons. Used with permission from the publisher.

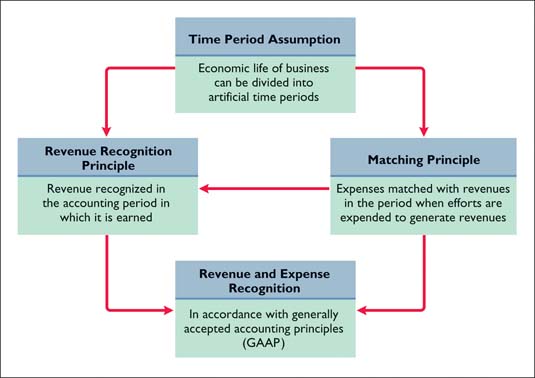

Most businesses need immediate feedback about how well they are doing. For example, management usually wants monthly reports on financial results, most large corporations are required to present quarterly and annual financial statements to stockholders, and the Internal Revenue Service requires all businesses to file annual tax returns. Accounting divides the economic life of a business into artificial time periods. This is the time period assumption. Accounting time periods are generally a month, a quarter, or a year.

Many business transactions affect more than one of these arbitrary time periods. For example, a new building purchased by Citigroup or a new airplane purchased by Delta Air Lines will be used for many years. It doesn't make sense to expense the full cost of the building or the airplane at the time of purchase because each will be used for many subsequent periods. Instead, we determine the impact of each transaction on specific accounting periods.

Determining the amount of revenues and expenses to report in a given accounting period can be difficult. Proper reporting requires an understanding of the nature of the company's business. Two principles are used as guidelines: the revenue recognition principle and the matching principle.

The Revenue Recognition Principle

|

|

|

|

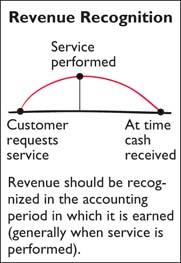

The revenue recognition principle requires that companies recognize revenue in the accounting period in which it is earned. In a service company, revenue is considered to be earned at the time the service is performed. To illustrate, assume Conrad Dry Cleaners cleans clothing on June 30, but customers do not claim and pay for their clothes until the first week of July. Under the revenue recognition principle, Conrad earns revenue in June when it performs the service, not in July when it receives the cash. At June 30 Conrad would report a receivable on its balance sheet and revenue in its income statement for the service performed.

The Matching Principle

In recognizing expenses, a simple rule is followed: “Let the expenses follow the revenues.” Thus, expense recognition is tied to revenue recognition. Applied to the preceding example, this means that the salary expense Conrad incurred in performing the cleaning service on June 30 should be reported in the same period in which it recognizes the service revenue. The critical issue in expense recognition is determining when the expense makes its contribution to revenue. This may or may not be the same period in which the expense is paid. If Conrad does not pay the salary incurred on June 30 until July, it would report salaries payable on its June 30 balance sheet.

The practice of expense recognition is referred to as the matching principle because it dictates that efforts (expenses) be matched with accomplishments (revenues). Illustration 1 shows these relationships.

|

|

|

|

||||||||||||||

|

|

|

|

|

|||||||||||||

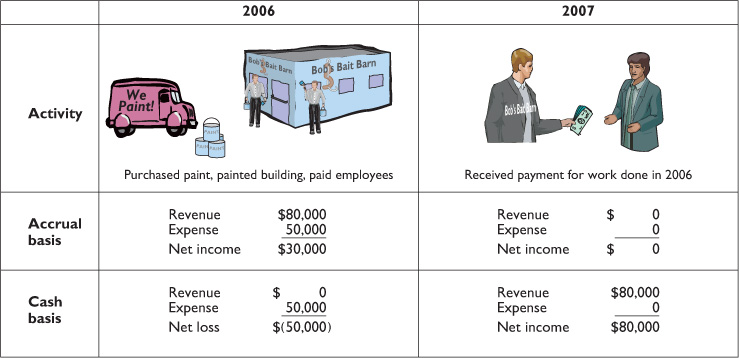

Accrual Accrual-basis accounting means that transactions that change a company's financial statements are recorded in the periods in which the events occur. For example, using the accrual basis means that companies recognize revenues when earned (the revenue recognition principle) rather than when they receive cash. Likewise, under the accrual basis, companies recognize expenses when incurred (the matching principle) rather than when paid.

An alternative to the accrual basis is the cash basis. Under cash-basis accounting, companies record revenue only when cash is received. They record expense only when cash is paid. The cash basis of accounting is prohibited under generally accepted accounting principles. Why? Because it does not record revenue when earned, thus violating the revenue recognition principle. Similarly, it does not record expenses when incurred, which violates the matching principle.

Illustration 2 compares accrual-based numbers and cash-based numbers. Suppose that Fresh Colors paints a large building in 2006. In 2006 it incurs and pays total expenses (salaries and paint costs) of $50,000. It bills the customer $80,000, but does not receive payment until 2007. On an accrual basis, Fresh Colors reports $80,000 of revenue during 2006 because that is when it is earned. The company matches expenses of $50,000 to the $80,000 of revenue. Thus, 2006 net income is $30,000 ($80,000 − $50,000). The $30,000 of net income reported for 2006 indicates the profitability of Fresh Colors' efforts during that period.

|

Illustration 2 |

Accrual versus cash basis accounting |

If, instead, Fresh Paint were to use cash-basis accounting, it would report $50,000 of expenses in 2006 and $80,000 of revenues during 2007. As shown in Illustration 2, it would report a loss of $50,000 in 2006 and would report net income of $80,000 in 2007. Clearly, the cash-basis measures are misleading because the financial performance of the company would be misstated for both 2006 and 2007.

02 DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION 029 BUREAU

02 DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION 031 BUREAU

02383 CHAPTER 3 02 DEPARTMENT OF FINANCIAL AND PROFESSIONAL

Tags: accounting topic, basis accounting, revenue, expense, reference, financial, topic, accounting, recognition

- SZANOWNI PAŃSTWO CHCIAŁBYM PRZEDE WSZYSTKIM PODZIĘKOWAĆ ORGANIZATOROM DZISIEJSZEGO SPOTKANIA

- ANNEXE 1 DONNÉES D’EXPÉRIENCE INTERNATIONALES SUR LES MÉCANISMES

- SITUATION OF HUMAN RIGHTS IN THE REPUBLIC OF BOSNIA

- R EGLES DE CLASSE INTERNATIONALES 10R 2 002 LA

- 2014 ANGIE’S LIST SUPER SERVICE AWARD® TRADEMARK USAGE STANDARDS

- 104A REUNIÓN DE LA CONFERENCIA INTERNACIONAL DEL TRABAJO (113

- BOROUGH OF BEACH HAVEN COUNTY OF OCEAN ORDINANCE 202015C

- UGOVOR O POSREDOVANJU U KUPOVINI NEPOKRETNOSTI ZAKLJUČEN DANA

- О К Р Ъ Ж Е Н С Ъ

- ENERGY STORAGE IRELAND MEMBERSHIP APPLICATION FORM 2020 (JAN –

- MEKANİK TESİSAT PROJE VE TEKNİK UYGULAMA SORUMLULUĞU HİZMETLERİ İÇİN

- GISA PLECS DE PRESCRIPCIONS GPLP 14V03 030106

- ŞIRINDERE İLETIŞIM VE EĞITIM PROJESI KARAKUSUNLAR MAHALLESI ŞIRINDERE BÖLGESINDEKI

- HASAR BİLDİRİM VE TAAHHÜT BELGESİ DOSYA NO …………………… TARIH………………

- REGULAMIN PIKNIKU RODZINNEGO ”BAJKOWY PIKNIK RODZINNY” W DNIU 04

- GIMNAZIJA ANTONA AŠKERCA ŠOLSKI CENTER LJUBLJANA SEVEN WONDERS OF

- LE TÉLÉTHON DES FRANÇAIS DE L’ÉTRANGER L’OBJECTIF L’IDÉE EST

- BESTILLING AV ELEVTRANSPORT SKOLEÅRET 20172018 SKJEMAET SENDES FERDIG UTFYLT

- TNRLW253 PÁGINA 0 ORGANIZACIÓN MUNDIAL DEL COMERCIO TNRLW253 21

- NHSSCOTLAND WORKFORCE ATTENDANCE POLICY STAGE 1 PAPER BASED APPEAL

- ARBOBELEIDSASPECTEN INHALATIE ALLERGENEN PREVENTIEF BELEID (OA INKOOPBELEID)

- FICHE N° 4 LE ROLE DES ORGANISATIONS INTERNATIONALES

- V12616 SUBSTANTIAL CURRICULUM CHANGE FORM (PRESENT ONLY ONE PROPOSED

- CIRCULAR Nº 29 DEL 04 DE JUNIO DE 1999

- HEALTH PROTECTION REQUIREMENTS FOR MINERAL WATER PASSED WITH THE

- IP 105 AGENDA ITEM CEP 4 E PRESENTED BY

- TV1000 BALKAN EET PENTRU INFORMAŢII SUPLIMENTARE VĂ RUGĂM SĂ

- POLICY ON RELEASE OF “RAW DATA” FROM PSYCHOLOGICAL AND

- UICN UNION INTERNATIONALE POUR LA CONSERVATION DE LA NATURE

- BEREDSKAPSPLAN FOR GULEN KOMMUNE FOTO FRÅ ØVING – BRANN

OPĆA BOLNICA VARAŽDIN BROJ 021265022017 DOKUMENTACIJA O NABAVI ZA

DIRECCIÓN JURÍDICA REGISTRO DE CONTRATOS 2014 PARA TRANSPARENCIA NO

DIRECCIÓN JURÍDICA REGISTRO DE CONTRATOS 2014 PARA TRANSPARENCIA NOZAŁĄCZNIK DO UCHWAŁY NR 312030409 ZARZĄDU WOJEWÓDZTWA MAZOWIECKIEGO Z

TABELAS DA NORMA DE QUALIDADE DA ÁGUA PARA CONSUMO

IZJAVA OZIROMA POOBLASTILO ZA PRIDOBITEV OSEBNIH PODATKOV SPODAJ PODPISANIA

………………………… Dnia……………… ………………………………………………… (imię i Nazwisko Zgłaszającego) ……………………………………………… ……………………………………………�

2 REUNIÓN PREPARATORIA DE LA SEGUNDA REUNIÓN

NOTA DE PRENSA TPA RETRANSMITE LAS FINALES DEL MEMORIAL

NOTA DE PRENSA TPA RETRANSMITE LAS FINALES DEL MEMORIALSUPPLEMENTARY MATERIAL PROTEIN CONTENT ( CRUDE PROTEIN) FOR

PRAVIDLA PRO ŘEŠENÍ VLASTNICKÝCH A UŽÍVACÍCH VZTAHŮ K POZEMNÍM

PRAVIDLA PRO ŘEŠENÍ VLASTNICKÝCH A UŽÍVACÍCH VZTAHŮ K POZEMNÍMRECORD OF COUNSELING SESSION NAME OF EMPLOYEE EMPLOYEE NUMBER

MENUS BANQUETES 2015 MENU Nº1 COCKTAIL DE BIENVENIDA BEBIDAS

CONVOCATÒRIA DE MATRÍCULA AL CENTRE EDUCATIU INFANTIL VERA DE

VALG AV REPRESENTANTER TIL GENERALFORSAMLINGEN FOR SJØMANNSKIRKENNORSK KIRKE I

TEAM MEMBER RATING SHEET EACH TEAM MEMBER SHOULD FILL

ANÀLISI DE LA DEMANDA EN PRIMERA PREFERÈNCIA CURS 20172018

ANÀLISI DE LA DEMANDA EN PRIMERA PREFERÈNCIA CURS 20172018 Nº PROCEDIMIENTO 030622 CÓDIGO SIACI SKKG CONSEJERÍA DE FOMENTO

Nº PROCEDIMIENTO 030622 CÓDIGO SIACI SKKG CONSEJERÍA DE FOMENTO TIPO A LAS RESPUESTAS CORRECTAS PUNTÚAN +050 Y LAS

TIPO A LAS RESPUESTAS CORRECTAS PUNTÚAN +050 Y LAS TRABAJO DE (SEGÚN PERTOQUE GRADOMÁSTER) GRADO EN INGENIERÍA ……

TRABAJO DE (SEGÚN PERTOQUE GRADOMÁSTER) GRADO EN INGENIERÍA ……ANEXO 7D2 CATALOGO DE CONCEPTOS NOVAUNIVERSITAS LICITACION PÚBLICA